You're profitable on paper. So why is your UA budget still capped?

TL;DR:

- Mobile apps can be profitable on paper and cash-constrained at the same time — App Store and Google Play pay out 30-45 days after a transaction

- Positive ROAS tells you the campaign works. It doesn't tell you whether the cash to scale it is actually in your account

- Traditional financing options weren't built around mobile cash flow cycles — they're too slow, too expensive, or too dilutive

- The solution isn't more revenue. It's faster access to revenue you've already earned

- Adapty Finance advances up to 85% of store revenue before the payout date, with no equity and no fixed repayments

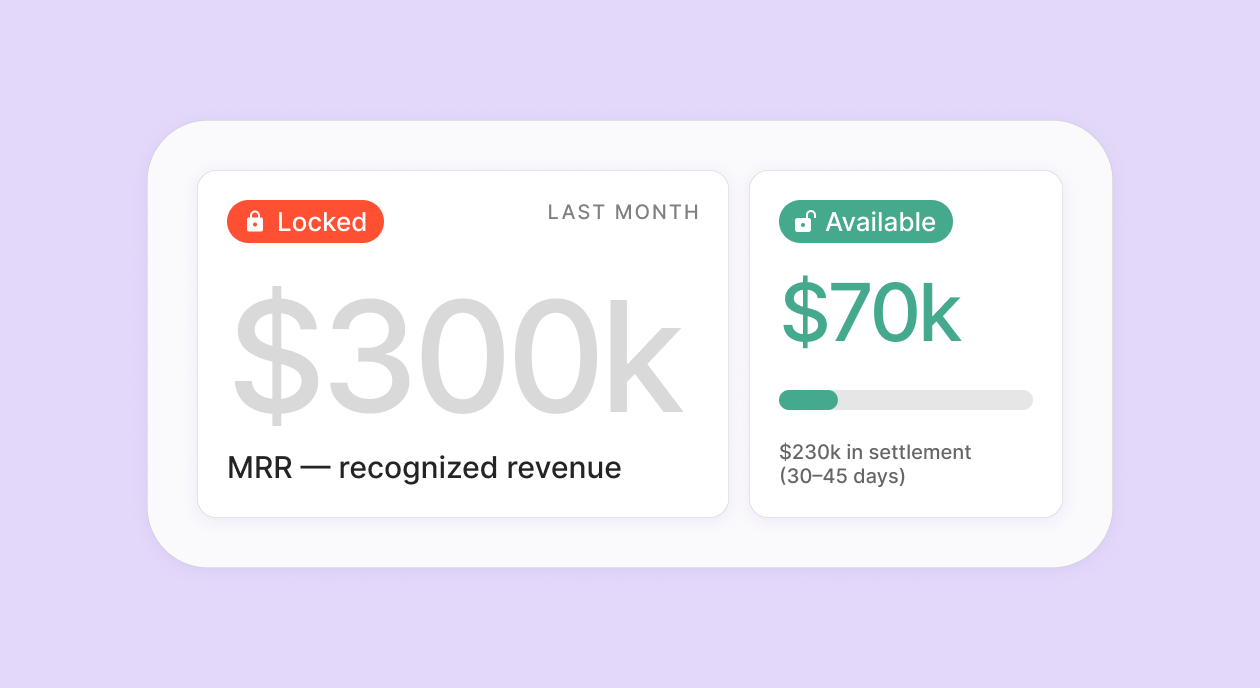

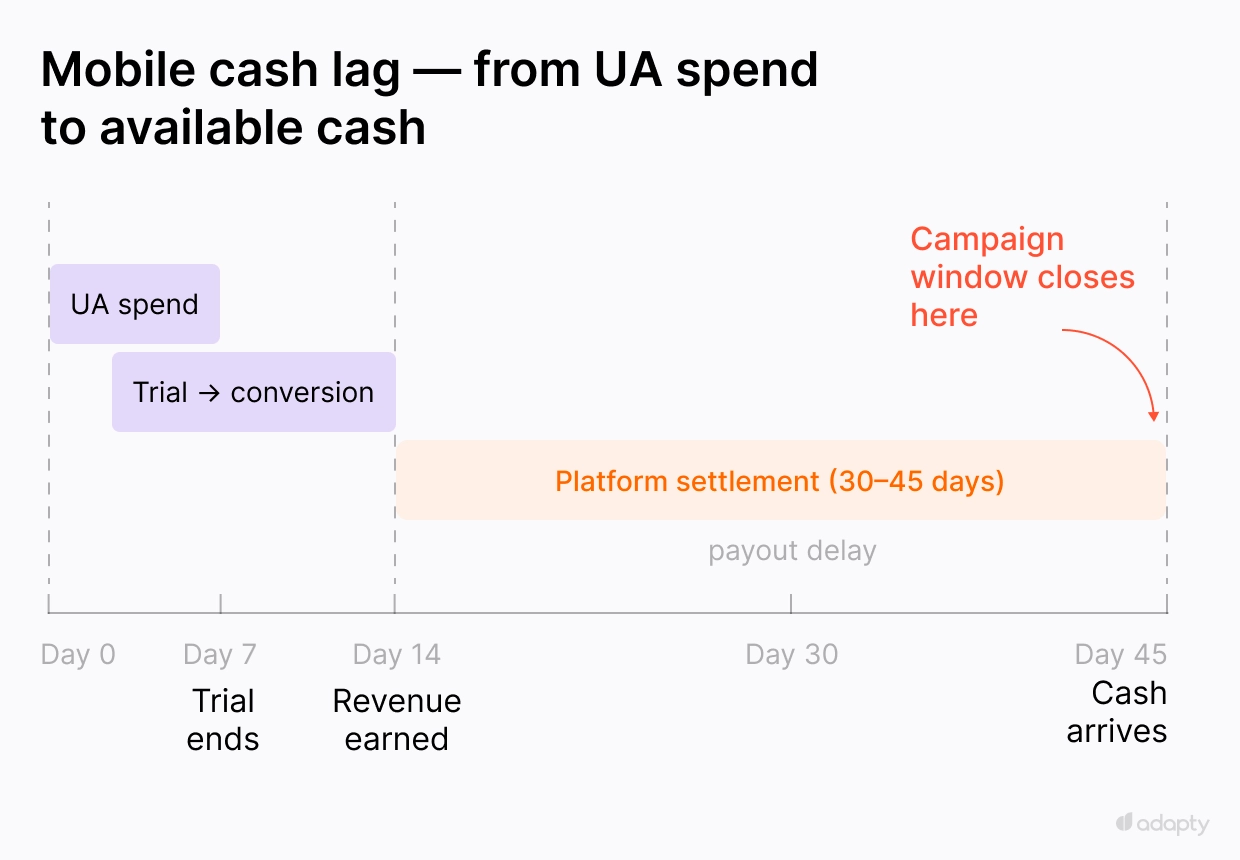

Managing a mobile app UA budget gets complicated fast when your bank account shows $70K and your MRR shows $300K. The remaining $230K is earned — it's sitting in settlement queues, moving through renewal cycles, waiting on platform processes. The App Store and Google Play typically pay out 30-45 days after a transaction, so by the time the money arrives, the campaign window you needed it for is long gone.

Your UA team found a campaign running at 150% ROAS two days ago. Everything checks out. The budget request came in yesterday, and you don't have the cash to fund it.

This is the mobile app UA budget problem that doesn't show up in your P&L — the revenue is real, the business model works, but the cash to act on the next opportunity hasn't arrived yet. Many mobile apps are profitable on paper, yet unable to reinvest into growth.

Why does profit look good when there's no cash to spend?

Most founders hit this wall at the same moment: the business is clearly working, and there still isn't enough cash to act on it. Revenue is in the dashboard. Profit looks fine, but cash — the number that actually decides whether you can run tomorrow's campaigns — is sitting somewhere between your users' payments and your bank account, moving through a settlement process on a schedule you don't control.

If your app earns $300K in MRR, that's not $300K available to spend this month. A portion hasn't been cleared yet. Renewals from last week are queued. Refunds are still being processed. In accounting terms this is accounts receivable — and for mobile apps it's not an edge case, it's how the entire revenue model works.

Growth decisions get made in cash. When you decide whether to double UA spend this week, you're looking at your bank balance, not your P&L. Two revenue numbers, one dashboard breaks down exactly why the number in your dashboard and the number in your bank account will never match.

Why do mobile apps run out of cash faster than SaaS?

SaaS companies billing via Stripe get paid within days of a transaction. Mobile apps don't have that luxury.

The cash lag in mobile compounds from three directions at once. UA spend goes out today — before the cohort generates a single dollar, sometimes weeks before. Users who install don't always convert immediately; trials run for 7 or 14 days, annual plans convert at lower rates, and revenue from today's spend often doesn't show up for a month. Then the platform holds the money for another 30-45 days before paying out.

On top of that, CPI moves like an auction. Competitor budgets spike around the new year, major launches, seasonal peaks — and your cost per install can jump 20-40% overnight. The window to scale opens and closes in days, while the cash to fund it arrives weeks later.

Why can't you scale UA campaigns even when ROAS is positive?

The frustration sits in one specific place: the UA team has the data, the campaigns are performing, and the budget still gets cut.

Your UA team identifies campaigns with ROAS above 100%. Creatives are working. The audience is responsive. CPI is acceptable. Every signal says: increase budget, capture the window, grow.

But the budget gets capped anyway — because there isn't enough cash available to fund the scale.

Finding winning campaigns is the easier part. Having the cash to scale them when the window is open is where most apps get stuck.

To make it concrete:

| Now | At scale | |

| Monthly subscription revenue | $250K | $250K |

| Revenue in transit | $180K | $180K |

| Available cash | $70K | $70K |

| UA spend needed | $80K | $200K |

| Can you fund it? | ✓ Yes | ✗ No |

Everything worked except the timing.

The timing problem gets worse during the highest-value windows — Q4, back-to-school, major seasonal peaks — exactly when CPI is highest and the cost of sitting on the sidelines is biggest. The ROAS calculation only holds if the underlying revenue data is clean — here's why most UA teams measure it against the wrong number.

Why don't bank loans, credit cards, or equity work for mobile growth?

The obvious response to a cash constraint is to find more capital — but the standard options weren't built around how mobile revenue actually moves.

| Speed | Cost | Equity lost | Built for mobile? | |

| Bank loan | Weeks / months | High friction | No | No |

| Credit card | Fast | High interest | No | No |

| Equity | Months | Ownership permanently | Yes | No |

| Revenue advance | 24 hours | Fee on advance | No | Yes |

- Bank loans are built for businesses with hard assets and predictable cash flow. Mobile apps have neither — what they have is recurring subscription revenue that arrives on a platform-controlled schedule. Approval takes weeks or months, lenders want collateral and financial history, and by the time funding arrives, the campaign window is gone.

- Credit cards move fast, but the cost compounds quietly. High interest rates erode the ROAS you're trying to protect, and credit limits don't scale with your actual revenue. Running significant UA spend on revolving credit is effectively a tax on growth.

- Equity solves a different problem entirely. Raising a round takes months, costs ownership permanently, and introduces investor expectations around burn and trajectory that don't align with a team trying to move fast on a UA opportunity. Here's what actually happens: you spend six months on fundraising, close a round, and the campaign window you needed capital for closed in week two.

None of these were designed for a business where the core constraint is a 30-45 day gap between earned revenue and available cash. The solution has to match the problem. For a full breakdown of non-dilutive options available to mobile apps, this guide covers five alternatives worth understanding before committing to any of them.

What's the missing layer between earned revenue and available cash?

For most mobile apps in this position, the gap between what's earned and what's available isn't a sign the business is struggling. It's a structural feature of how platform payouts work.

Working capital — in the context of mobile apps — means bridging that gap. Getting access to earned revenue before the platform pays it out, so you can deploy it when growth opportunities require it.

In traditional industries, businesses have used working capital financing for decades to smooth cash flow between when value is created and when it's received. Mobile apps generate a new form of accounts receivable — predictable, subscription-driven revenue locked in settlement cycles. The infrastructure to access it on your own schedule is what's been missing.

How do fast-growing apps scale UA without hitting a cash ceiling?

The apps that scale consistently don't wait on the platform payout schedule — they access earned revenue earlier and redeploy it into UA within the same week, effectively running four reinvestment cycles a month instead of one.

The math compounds quickly. An app reinvesting $60K every week generates four times the UA cycles of an app waiting on the standard 30-45 day payout, and over a quarter that difference in velocity shows up in growth numbers in a way that's hard to close from behind.

Accessing it earlier doesn't require a different business model or outside capital — it requires closing the gap between when revenue is earned and when it actually arrives. Paywall conversion is the other side of the same equation — faster reinvestment only compounds if the paywall is performing. Here's how to run paywall A/B testing without a dedicated growth team.

How does Adapty Finance close the gap between earned revenue and available cash?

Adapty Finance works with App Store and Google Play revenue that's already in the settlement pipeline — money your subscribers have paid, but that hasn't landed in your account yet.

You receive up to 85% of that revenue before the platform pays it out. When the store settles, repayment happens automatically against the incoming payout. For a UA team sitting on positive ROAS data and a capped budget, the timing gap stops being the deciding factor — the campaigns that were ready to scale last week can actually scale this week.

Calculate your available advance

You already know which campaigns you'd scale. The only question is how much of your earned revenue is currently sitting in settlement — and whether you can access it before the window closes. See how much of your revenue is locked — and how much you could unlock.