TL;DR

- Google Play confirmed its rollout on June 24. For the US, UK, and EEA, the new structure starts June 30, 2026.

- You can now sell through your own billing or send users to a web checkout, alongside Google Play Billing.

- Google split the service fee from the billing fee. Subscriptions carry a 10% service fee, plus 5% when you use Google Play Billing.

- Route payments through alternative billing or a web link, and Google’s cut drops to 10%, with your own processor taking its share from there.

- New Apps Experience and Games Level Up programs open at lower rates for qualifying apps from September 30, 2026.

On June 24, Google Play confirmed the dates on a change it announced back in March. Starting June 30 in the US, UK, and EEA, you can take subscription payments through your own system or send users to a web checkout, instead of running everything through Google Play Billing. For anyone who has treated Android as the platform with all the users and none of the margin, that’s worth a fresh look.

It’s the most open the Play Store has been since launch, and it follows Google’s settlement with Epic. Whether the flexibility shows up in your revenue depends on what you do with it.

What did Google open up?

Google changed two things.

- You can now process payments through another provider or send users to your own website to check out, instead of running every transaction through Google Play Billing. If you’d rather not use Google’s default purchase screen, you can design your own under its UX guidelines.

- And Google pulled the billing fee out of the service fee, so you only pay for billing when you use Google’s system.

Here is how that plays out on subscriptions in the US, UK, and EEA:

| Your setup | Service fee | Billing fee | Google’s total cut |

|---|---|---|---|

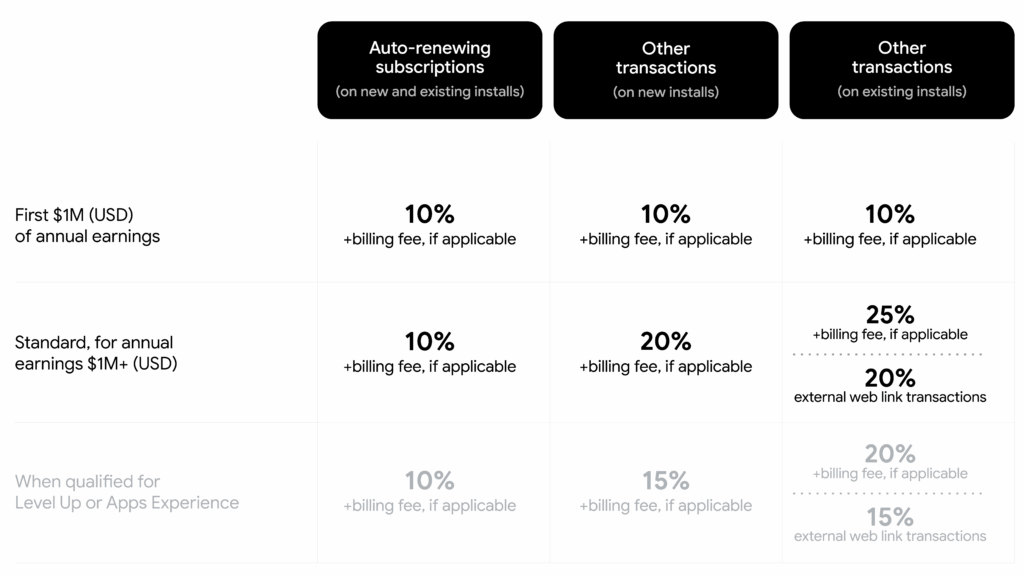

| Google Play Billing | 10% | 5% | 15% |

| Alternative billing or web link | 10% | 0% | 10% + your processor |

For most subscription apps, the total doesn’t move. The 10% service fee covers every auto-renewing subscription, at any revenue level. Use Google’s billing, and the 5% billing fee lands on top, putting you back at 15%, the same rate in place since January 2022. You reach 10% only by moving payments to your own checkout, and there your processor takes its share.

Whether that’s worth it comes down to your processor’s fee. On a $9.99 monthly plan, a card processor’s fixed fee per transaction can eat most of what you saved by skipping Google’s 5%. On a $99.99 annual renewal, the processor’s percentage comes in under 5%, so you keep the difference. The higher the price and the longer the plan, the more it pays to move off Google’s billing. Cheap monthly plans usually aren’t worth the switch.

Two caveats. This applies to the US, UK, and EEA from June 30, with Australia, Japan, and Korea by the end of 2026, and the rest of the world from September 2027. And the new-install versus existing-install tiers you’ve seen quoted apply only to one-time purchases, so they don’t touch your subscription math here.

For the full picture, here is Google’s rate card. Auto-renewing subscriptions are 10% on every tier and install type, so the only rates that change are for one-time purchases.

Add the 5% billing fee (US, UK, EEA) when you use Google Play Billing. On existing installs, a web link runs cheaper than Google’s billing.

Why does this count as a step toward developers?

For years, selling on a big app store meant using its billing and playing by its rules. Google just relaxed both. Now you can take payment whichever way works best for your margins, and point users to a web checkout to keep more of what they spend.

The gap with Apple is wide right now. Apple has spent its regulatory years defending its model, giving up as little as it can and still charging wherever courts let it. Google went the other way, settling with Epic and cutting its fees, with a dated rollout schedule to match. Whatever’s driving it, app developers come out ahead.

On its own, none of this changes your economics. It gives you options. Whether they show up in revenue comes down to the funnel you build behind them.

How fast is Android changing?

Faster than its reputation. The platform developers filed under high-traffic and low-yield are moving, and the 2026 State of in-app subscriptions data shows it in three places.

1. Users are starting to pay. For the first time, install-to-paid on monthly subscriptions reached iOS and Android parity in the Entertainment category, an early sign that Android users in some niches are ready to convert.

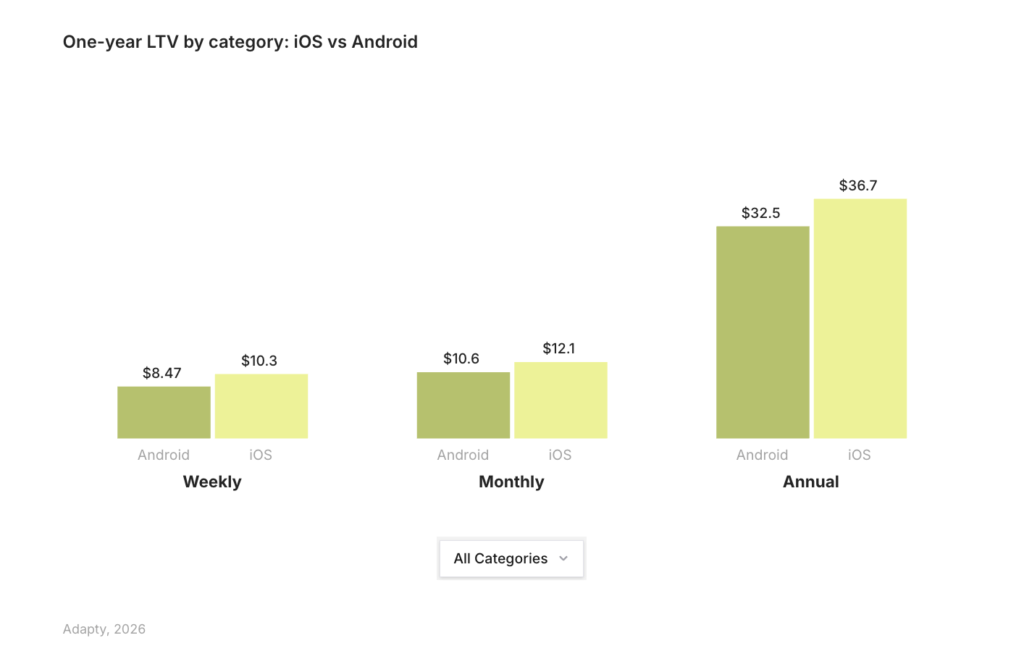

2. The ones who convert are nearly as valuable. One-year LTV runs close across platforms, $32.5 on Android against $36.7 on iOS for annual plans, about 11% apart. The value behind an Android subscriber is already there.

Is Google Play worth your time now?

Plenty of teams still think Android users don’t spend, and that paid traffic never pays back there. It’s not true anymore, and the people running both stores see why.

The App Store has gotten crowded and slow. It’s full of quick AI-built apps, and a review can take weeks. Apple also bans and rejects more than it used to. Google Play is easier right now. Apps get approved faster and get rejected less. Bans are rare. There’s less competition in a lot of categories, and Google pays sooner, around the 15th for the month before, about two to three weeks ahead of Apple.

At scale, the apps that do well build Android as its own product, with its own playbook. A conversion on iOS is still worth more in raw dollars, so the approach has to differ. Teams use a rough rule. Once your iOS app passes $30K MRR, an Android version often adds another $10K to $20K, around 10% to 50% of what iOS makes.

Buying traffic works differently for each store. On iOS, the math works almost everywhere, so you run most countries and block a few. On Android, you usually pick your countries, leaning on the US and other Tier 1 markets, though some Tier 3 ones surprise you. Watch your refunds. Once they pass 8% to 10%, you’re in risk territory, and moving spend back to the US usually steadies things, since US refunds tend to run much lower.

None of this settles it for your app. It just shows where the upside is. The fee change alone won’t move your revenue; what moves it is taking Android seriously as a place people are starting to pay, and building the funnel to match.